Table of Contents

Table of Contents

- GLBA Compliance Software Guide: How to Choose a Platform for the Safeguards Rule

- What Is GLBA Compliance Software?

- What GLBA Compliance Software Does

- Why Organizations Need GLBA Compliance Tools

- Types of GLBA Compliance Tools

- Capability Requirements for GLBA Compliance Software

- What to Look for in GLBA Compliance Software

- How to Compare GLBA Compliance Tools

- Best GLBA Compliance Tools

- How to Simplify GLBA Compliance

- Key Takeaways

-

GLBA Compliance Software FAQs

- Is GLBA compliance software required?

- What does GLBA compliance software cost?

- Does GLBA apply to non-banking organizations?

- What’s the difference between GLBA compliance software and general GRC software?

- How long does GLBA compliance software take to deploy?

- Which examiners review GLBA compliance program documentation?

GLBA Compliance Software Guide: How to Choose a Platform for the Safeguards Rule

GLBA compliance software helps financial institutions and non-banking covered entities satisfy the Safeguards Rulerequirements for written risk assessments, vendor oversight, employee training, and ongoing monitoring — without building each workflow from scratch.

The GLBA Safeguards Rule applies to banks and credit unions, but it also covers mortgage brokers, automobile dealers, accountants, tax preparers, and other entities handling consumer financial information. Because most of these organizations run lean compliance teams, a GLBA platform that consolidates the §314.4 requirements into one workflow is the best fit.

This guide explains what GLBA compliance software does, why organizations need it, the platform categories most organizations evaluate, with capability requirements, evaluation criteria, and recommendations by institution type.

What Is GLBA Compliance Software?

GLBA compliance software is a category of governance, risk, and compliance (GRC) tooling that helps organizations satisfy requirements for the Gramm-Leach-Bliley Act Safeguards Rule. It consolidates §314.4 workflows — risk assessment, vendor oversight, employee training, ongoing monitoring, and incident response — into a single platform that mimics how examiners actually review Safeguards Rule programs.

GLBA compliance software is a type of GRC tool that helps organizations satisfy the GLBA Safeguards Rule‘s §314.4 requirements for risk assessment, vendor oversight, training, and ongoing monitoring.

The platform category fits financial institutions and non-banking GLBA-regulated entities that need examiner-grade documentation, including banks, credit unions, mortgage brokers, accountants, automobile dealers, and tax preparers.

What GLBA Compliance Software Does

GLBA compliance software operationalizes the core Safeguards Rule workflows that §314.4 requires of covered organizations. Often, that includes:

- Written risk assessment (§314.4(b)): Periodic identification and documentation of foreseeable risks to customer information.

- Vendor and TPRM oversight (§314.4(f)): Due diligence, contract review, and ongoing monitoring of service providers handling customer information.

- Training records (§314.4(e)): Completion tracking, attestations, and role-based curriculum mapping for personnel.

- Ongoing monitoring and incident response (§314.4(d), (g), (h)): Regular testing of safeguards, periodic evaluation and program adjustment based on monitoring results, and incident workflow with evidence trail.

The category sits within broader financial services compliance software. The differentiator is evidence structure: GLBA-specific tools are organized around §314.4 subsections, which is what FTC, FFIEC, and NCUA examiners look for during program review.

Any organization that falls within the Safeguards Rule’s definition of “financial institution” needs GLBA compliance software. Institutions handling customer information on fewer than 5,000 consumers fall under the §314.6 exemption from written risk assessment, penetration testing, and board reporting requirements. The workflow need still exists, but evidence formality scales with consumer volume.

The 2021 amendment expanded enforcement scope and specified subsection-level requirements that practically require workflow tooling at any meaningful volume of customer data or third-party relationships. GLBA’s other half — the Privacy Rule — sits outside Safeguards Rule software scope.

Why Organizations Need GLBA Compliance Tools

GLBA-regulated organizations need compliance tooling because §314.4 has outgrown spreadsheets. Examiners now expect subsection-mapped evidence on demand, and the consequences for thin documentation have sharpened.

Framework Scale

§314.4 spans 10 subsections covering risk assessment, technical safeguards, testing, training, vendor oversight, program updates, incident response, board reporting, and breach notification. Each subsection produces its own evidence trail. A platform that doesn’t organize artifacts by subsection forces compliance teams to reassemble evidence from scratch during examinations.

Spreadsheet Limits

Spreadsheets can carry a single-cycle risk assessment for a small institution. They cannot maintain version history that examiners can follow, vendor lifecycle state across hundreds of providers, training attestations tied to role, or the breach-notification clock under §314.4(j). The failure mode shows up first in vendor oversight, where third-party incidents now drive the majority of reportable events.

Regulatory Pressure

The FTC’s 2021 amendment specified §314.4 requirements at the subsection level. The May 2024 notification rule added a 30-day reporting clock with no harm threshold. The FFIEC CAT sunset in August 2025 reshaped how banks demonstrate cyber-risk posture. NCUA’s 72-hour cyber incident notification rule applies in parallel for credit unions. Programs that can’t surface evidence in the formats examiners expect carry real enforcement exposure.

Decentralized IT and Shadow Vendor Risk

Mid-market FIs and non-banking regulated entities rarely run centralized IT. Vendor relationships live across departments — payments, marketing, lending operations, HR — and consumer-facing data flows touch processors the central security team didn’t onboard. Compliance tools that can’t ingest vendor inventories from multiple owners leave §314.4(f) exposure unsurfaced until an incident forces discovery.

Types of GLBA Compliance Tools

GLBA compliance tools fall into four categories: enterprise GRC platforms, GRC Assessment Platforms™, compliance automation suites, and DIY spreadsheets. Buyer profile, deployment model, and depth of §314.4 evidence coverage separate them, and most institutions evaluate two or three before settling.

Enterprise GRC Platforms

Enterprise GRC platforms target large, multi-framework programs at Fortune 500 banks, insurers, and capital markets firms. They cover GLBA alongside SOX, Basel III, FFIEC, NYDFS 23 NYCRR 500, and dozens of other frameworks at depth. Deployment timelines span quarters to a year, with significant professional-services investment and dedicated GRC headcount.

Examples: RSA Archer, MetricStream, ServiceNow GRC, IBM OpenPages.

GRC Assessment Platforms™

GRC Assessment Platforms™ purpose-build for IT and vendor risk assessment workflows at mid-market organizations. They focus on the questionnaire → control → framework → risk lineage that §314.4 evidence depends on, with no-code configuration and weeks-to-deploy timelines. Examiner-grade reporting on §314.4 subsections sits inside the workflow rather than as a separate reporting build.

Examples: Isora GRC.

Compliance Automation Suites

Compliance automation suites target SaaS companies pursuing SOC 2, ISO 27001, and HIPAA reports. They emphasize continuous control monitoring against pre-built control libraries and auditor-facing dashboards. The audit model differs from §314.4 examination — these tools can supplement a GLBA program but rarely serve as the primary platform.

Examples: Drata, Vanta, Secureframe, Thoropass.

DIY Spreadsheets and SharePoint

Spreadsheet- and SharePoint-based programs persist at the smallest GLBA-regulated entities, especially those operating under the §314.6 small-entity exemption. They work for single-cycle assessments and low vendor counts. They break under examination cycles that require reproducible evidence across multiple §314.4 subsections.

Examples: Excel, Google Sheets, SharePoint document libraries.

Capability Requirements for GLBA Compliance Software

GLBA compliance software needs five core capabilities: written risk assessment, vendor oversight, training records, ongoing monitoring and incident response, and integration with the systems where customer information already lives. Each capability maps to a §314.4 subsection and forms a baseline requirement for evaluating any GLBA software vendor.

Written Risk Assessment (§314.4(b))

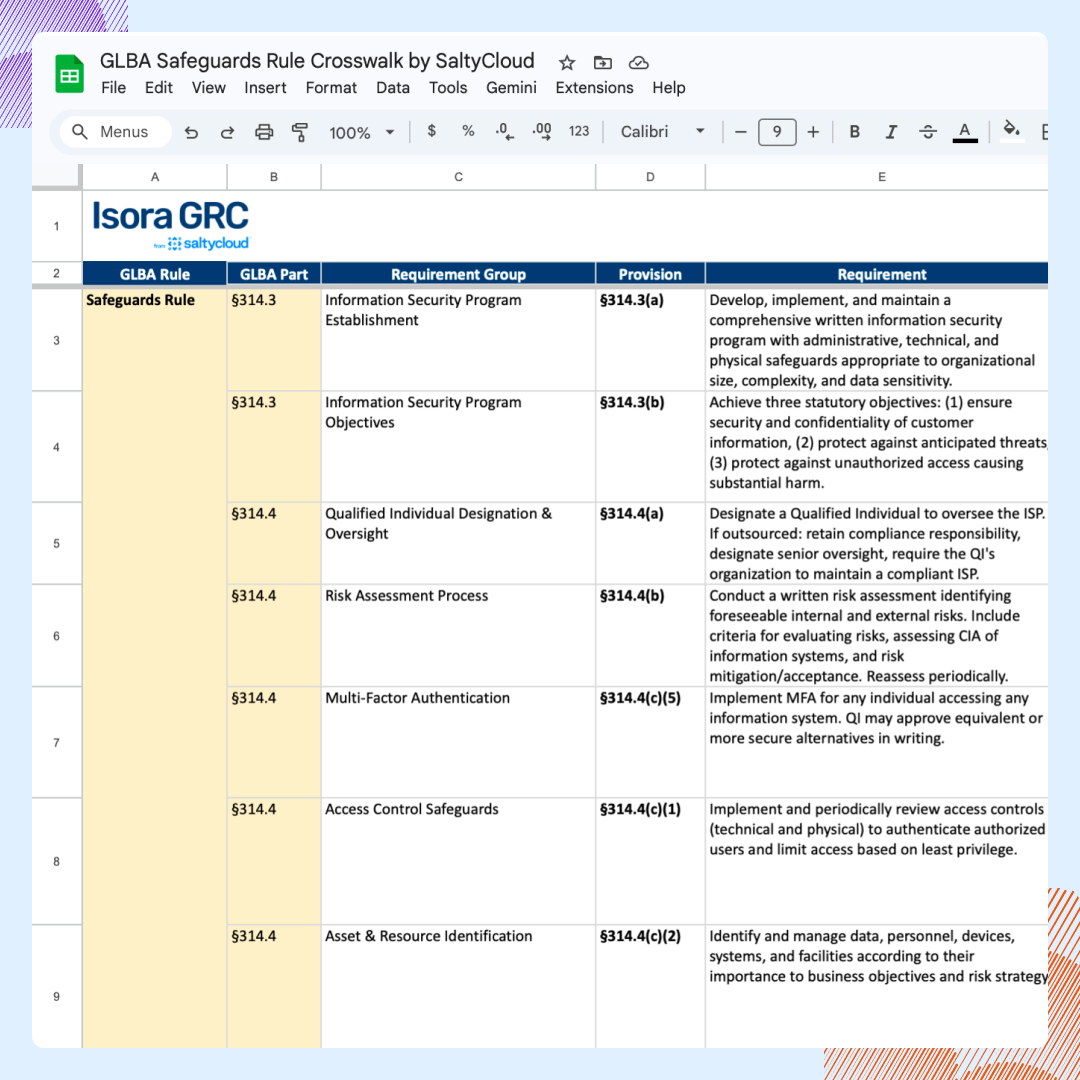

Section 314.4(b) requires identifying reasonably foreseeable internal and external risks to the security, confidentiality, and integrity of customer information. The assessment must specify how those risks will be managed and must be updated as conditions change.

Platform requirements: a configurable risk register, control mapping to §314.4 safeguards, a periodic review cadence, and version history showing when assessments were updated and by whom. See the GLBA risk assessment guide for the regulatory deep-dive.

Vendor Oversight (§314.4(f))

Section 314.4(f) requires due diligence in selecting service providers, contractual safeguards for customer information, and ongoing monitoring throughout the relationship.

OCC, Federal Reserve, and FDIC supervised institutions overlay Interagency Guidance on Third-Party Relationships: Risk Management (effective June 2023), which rescinded prior agency-specific guidance and applies a lifecycle-risk framework to the same vendor population. The NCUA’s 2024 Annual Report to Congress logged 892 reported cyber incidents from September 2023 through May 2024, roughly 73% tied to third parties — a quantified signal of where examiner attention concentrates.

Platform requirements: a vendor inventory, due-diligence questionnaire workflow, contract review tracking, ongoing-monitoring cadence configured by risk tier, and termination evidence. For institution-type-specific TPRM considerations, see GRC software for banks and credit unions.

Training Records (§314.4(e))

Section 314.4(e) requires documented completion of personnel training on the information security program, with particular attention to staff who access customer information directly.

Platform requirements: completion tracking, attestation records, and role-based curriculum mapping so training assignments match each employee’s actual responsibilities.

Ongoing Monitoring and Incident Response (§314.4(d), (g), (h))

Sections 314.4(d), (g), and (h) cover regular testing and monitoring of safeguards (d), periodic evaluation and program adjustment based on monitoring results (g), and written incident response procedures with board reporting (h). Section 314.4(d) sets the testing cadence — annual penetration tests and biannual vulnerability assessments, unless continuous monitoring substitutes. See GLBA cybersecurity requirements for the underlying technical controls.

Platform requirements: a control-monitoring workflow, periodic-test scheduling, a program-adjustment review cycle that captures monitoring findings and resulting program changes, and an incident workflow that captures detection, containment, recovery, and post-incident review artifacts.

Integration with Existing Systems

GLBA compliance software has to connect to the upstream systems where customer information already lives, including HRIS, asset inventory, network monitoring, and contract management. §314.4 evidence depends on data drawn from each of these, and platforms that can’t sync force compliance staff into manual data entry that breaks under examination scale.

Platform requirements: HRIS integration for training records and personnel data (§314.4(e)); asset inventory and CMDB integration for the technical scope of the program (§314.4(b), (c)); network and security monitoring integration for control evidence (§314.4(d)); and contract lifecycle management integration for vendor oversight artifacts (§314.4(f)). Open APIs and pre-built connectors matter more than proprietary integrations that lock the program into a single vendor stack.

GLBA Software Capability Checklist

The GLBA compliance software capability requirements checklist below maps each platform capability to its Safeguards Rule subsection and the specific functionality the platform must support. It covers §314.4(b), (e), (f), (d), (g), and (h) plus the cross-cutting requirements for examiner-evidence reporting and upstream system integration, and serves as a baseline scoring rubric for vendor evaluation.

| Safeguards Rule Requirement | Platform Capability |

| Written risk assessment – §314.4(b) | Configurable risk register, control mapping, version history |

| Vendor oversight – §314.4(f) | Vendor inventory, due-diligence workflow, ongoing monitoring, termination evidence |

| Training records – §314.4(e) | Completion tracking, attestations, role-based curriculum |

| Ongoing monitoring and testing – §314.4(d) | Control monitoring, periodic testing |

| Program evaluation and adjustment – §314.4(g) | Continuous program update based on monitoring findings, board reporting |

| Incident response – §314.4(h) | Incident workflow with evidence trail |

| Examiner-evidence reporting | Reproducible artifacts for FTC, FFIEC, NCUA, and state regulator review |

| Integration with existing systems | HRIS, asset inventory, network monitoring, and contract management connectors |

What to Look for in GLBA Compliance Software

The most important evaluation criteria are examiner-evidence readiness, framework portfolio coverage, vendor lifecycle scope, deployment timeline, staffing model fit, integration depth, scalability, and regulatory currency. Each maps to what FTC, FFIEC, and NCUA examiners check during program review and to the operational realities of running a GLBA program inside a lean compliance team.

| Criteria | Why It Matters | Questions to Ask Vendors |

| Examiner-evidence readiness | Examination cycles aren’t the time to discover that evidence has to be reassembled manually from spreadsheets. | Can the platform produce reproducible reports for FTC, FFIEC member agencies, NCUA, and state regulators on demand? |

| Framework portfolio coverage | GLBA standalone is rare in practice — most regulated FIs need it mapped alongside FFIEC, NCUA Part 748, NIST CSF 2.0, and state regulator frameworks. | Which frameworks ship pre-built? How is crosswalking handled when a new framework enters the program? |

| Vendor lifecycle scope | §314.4(f) covers due diligence, contract review, ongoing monitoring, and termination — not just questionnaire send-out. | Does the platform track every lifecycle stage in one system of record? How does ongoing-monitoring cadence vary by risk tier? |

| Deployment timeline | Small FIs and non-banking entities typically can’t absorb multi-quarter implementations. | What’s the time from contract to first examination-ready report? How much IT and professional-services overhead does setup require? |

| Staffing model fit and ease of use | Many GLBA programs are owned by non-GRC practitioners — compliance officers, ops leads, controllers — with zero to one dedicated compliance staffer. | Is the platform configuration-led or consulting-heavy? Can a non-specialist administer it without daily IT support? What does the learning curve look like for new users? |

| Integration depth | Customer information already lives in HRIS, asset inventory, network monitoring, and contract management systems; §314.4 evidence depends on data drawn from each. | Which pre-built connectors ship? Are open APIs available? How are integrations maintained as upstream systems change? |

| Scalability | Programs grow as institutions add vendors, expand into new business lines, layer on additional regulatory frameworks, and onboard more users. | Does the platform scale across vendor count, consumer volume, framework portfolio, and user count without forcing migration at the next inflection point? |

| Regulatory currency | The Safeguards Rule was amended in 2021, breach notification took effect in May 2024, and the FFIEC CAT sunset in August 2025 — frameworks move. | How does the vendor surface regulatory updates in the workflow? What’s the cadence for content refresh against framework changes? |

Notably, two of the criteria above tend to get less attention than they deserve. They are:

- Staffing model fit and ease of use: What determine whether a platform survives the second year — consulting-heavy implementations rebuild themselves into bottlenecks as the original integrator rolls off, and platforms that assume GRC-specialist users break down once a controller or ops lead inherits the program.

- Regulatory currency: What separates platforms that stay current from those that ship a 2021 baseline and expect customers to track changes themselves.

The May 2024 breach notification rule and the FFIEC CAT sunset in August 2025 — which moved bank examiner expectations to NIST CSF 2.0, CISA CPG 2.0, CRI Profile, or CIS Controls while credit unions continue to use the NCUA’s Automated Cybersecurity Examination Tool — both surfaced this divide in real time.

For community banks ($1B–$10B) and credit unions running multi-regulator programs, see GLBA tools and solutions for community banks and credit unions. For institution-type-specific guidance covering regional banks and other financial institutions, see GRC software for banks and credit unions.

How to Compare GLBA Compliance Tools

Most institutions compare GLBA compliance tools across three reference categories: Enterprise GRC, GRC Assessment Platforms™, and DIY spreadsheets. Feature-level comparisons miss the structural differences between them, and compliance automation suites sit out of this table because they operate under a different audit model (SOC 2, ISO 27001) and don’t produce §314.4 subsection evidence as a primary output.

| Enterprise GRC | GRC Assessment Platforms™ | DIY Spreadsheets | |

| Buyer profile | Fortune 500 banks, insurers, capital markets | Mid-market FIs, credit unions, non-banking entities | Single-staff programs, sub-5,000-consumer entities |

| §314.4 coverage | Full subsection coverage at depth | Full subsection coverage configured by use case | Partial — risk assessment and vendor inventory only |

| Vendor lifecycle | End-to-end with deep TPRM modules | End-to-end in one inventory system | Manual tracking; breaks above ~25 vendors |

| Deployment | 6–12 months with professional services | Days to weeks, no-code | Days, but breaks under examination |

| Staffing fit | Dedicated GRC team (5+ FTE) | Single compliance owner workable | Single compliance owner only |

| Examiner-evidence reporting | Configurable but report-build heavy | Built into workflow | Manual reassembly each cycle |

| Regulatory currency | Quarterly framework updates typical | Continuous framework updates | Customer maintains |

Compliance automation suites (Drata, Vanta, Secureframe) appear in adjacent buyer conversations and can supplement a GLBA program for SaaS-adjacent controls, but the audit-model mismatch — SOC 2 attestation versus FTC and FFIEC examination — keeps them out of the primary comparison set.

Best GLBA Compliance Tools

Isora GRC, RSA Archer, MetricStream, and Drata lead the GLBA compliance software market, with each vendor fitting a different institution profile. Institution type, asset size, staffing model, vendor count, and regulatory framework portfolio determine which platform category and which specific vendor fits. The table below maps recommended platforms to the organizations most often shopping for GLBA software.

| Organization Type | Best GLBA Tool | Rationale |

| Community banks ($1B–$10B) | GRC Assessment Platform™ | Community bank GLBA programs split between FFIEC IT examination and §314.4 subsection evidence under lean staff. The GRC Assessment Platform™ category consolidates both into one workflow — vendor inventory, risk register, and examiner-ready reports in one system of record — without the enterprise GRC implementation overhead that stalls in mid-market deployments. |

| Credit unions | GRC Assessment Platform™ | NCUA Part 748 layers onto GLBA, with the 72-hour cyber incident notification rule and ACET continuing in use after the FFIEC CAT sunset. Isora GRC ships pre-built GLBA and NIST CSF 2.0 questionnaires, an incident workflow that fits the 72-hour clock, and a non-GRC-practitioner UX that survives ownership by a controller or operations lead. |

| Non-banking GLBA-regulated entities | GRC Assessment Platform™ | FTC examination under 16 CFR Part 314 with no dedicated compliance headcount. Configuration-led deployment, the FTC’s subsection-mapped evidence categories built into the workflow, and the §314.6 exemption decision surfacing in scope — the same platform that runs a sub-5,000-consumer program also scales if consumer counts cross the threshold. |

| Regional banks | GRC Assessment Platform™ | Multi-regulator overlay (FFIEC + state banking departments + NYDFS 23 NYCRR 500 where applicable) with multi-hundred vendor populations. One risk register crosswalks GLBA, NIST CSF 2.0, NYDFS, and state regulator frameworks, and vendor lifecycle depth covers due diligence through termination across the full vendor count. |

Best Tool for Mid-Market GLBA-Regulated Entities: Isora GRC

Isora GRC is the GRC Assessment Platform™ — purpose-built for information security teams running GLBA, FFIEC, NCUA, and state regulator obligations in one shared workspace. Its configuration-led deployment is often the best fit for mid-market FIs and non-banking regulated entities running lean compliance teams.

In Isora, assessments, vendor inventory, asset inventory, risk register, exceptions, and examiner-ready reports are all connected. Findings from §314.4(b) written risk assessments flow directly into the risk register with full lineage, and vendor due-diligence under §314.4(f) sits in the same system of record as ongoing-monitoring evidence.

Where it fits: community banks ($1B–$10B), credit unions, regional banks running multi-regulator programs, and non-banking GLBA-regulated entities.

Best Tool for Fortune 500 Multi-Framework Programs: RSA Archer

Archer (RSA Archer) is an enterprise GRC platform built for Fortune 500 banks, insurers, and capital markets firms running dozens of frameworks at depth — SOX, Basel III, FFIEC, NYDFS, GLBA, and beyond. Its strength is framework portfolio breadth and configurability. The cost? Multi-quarter implementations with significant professional-services investment.

Meanwhile, many mid-market FIs and non-banking regulated entities who do buy Archer never fully deploy it. Today, this behavior surfaces as the stalled enterprise GRC pattern compliance teams describe at peer benchmarking sessions.

For institutions that need a security-team-owned workflow for §314.4(b) and (f) running inside a broader enterprise program, Isora GRC supplements Archer or replaces it where the staffing model can’t support enterprise implementation timelines.

Best Tool for Enterprise GRC with Deep FFIEC overlay: MetricStream

MetricStream is an enterprise GRC platform with deep FFIEC, OCC, and federal banking regulator overlays. Its the strongest fit for large banks running integrated risk management across operational risk, regulatory compliance, and IT GRC under one roof. The platform supports §314.4 subsection evidence at depth but, like other enterprise GRC suites, requires dedicated GRC headcount and a quarters-long implementation.

For institutions where GLBA sits inside a broader integrated risk program with 5+ FTE running it, MetricStream is a category fit. For mid-market FIs and non-banking entities where GLBA is the primary compliance driver and the team is lean, the GRC Assessment Platform™ category usually fits the workflow better.

Best Tool for SaaS-Adjacent GLBA Programs: Drata

Drata is a compliance automation suite built for SaaS companies pursuing SOC 2, ISO 27001, and HIPAA reports with continuous control monitoring against pre-built control libraries and auditor-facing dashboards. Its audit model is the differentiator and the limit — SOC 2 attestation differs from FTC, FFIEC, and NCUA examination in evidence structure, subsection mapping, and what regulators look for during program review.

For GLBA-regulated SaaS companies (fintech infrastructure, lending platforms, financial data processors), Drata can supplement adjacent SOC 2 controls and CI/CD-tied evidence. But it doesn’t substitute for the §314.4 subsection evidence categories examiners check during a Safeguards Rule review.

Most institutions pair Drata for SOC 2 with a GRC Assessment Platform™ like Isora GRC for GLBA, rather than treating either as the single source of truth.

How to Simplify GLBA Compliance

Isora GRC’s GRC Assessment Platform™ consolidates §314.4 written risk assessments, vendor oversight, training records, and examiner-ready reporting into one workspace. Purpose-built for information security teams to run and operationalize assessments as the foundation of GLBA risk and compliance, Isora fits financial institutions and non-banking regulated entities managing GLBA alongside adjacent obligations (FFIEC, NCUA, state regulators) under lean headcount.

Assessment Management

Isora GRC organizes the §314.4(b) written risk assessment as a campaign — questionnaire scoping, participant assignment, progress tracking, and series grouping by compliance goal. That way, a single compliance owner can run the assessment across departments without rebuilding the workflow each cycle. Series grouping lets an institution run §314.4(b) alongside vendor due-diligence (§314.4(f)) and personnel training (§314.4(e)) campaigns in one view. And, it goes live in days or weeks with no-code setup.

Questionnaires & Surveys

In Isora GRC, a questionnaire engine handles personnel training attestations under §314.4(e) and vendor due-diligence under §314.4(f) in the same workflow. Pre-built questionnaires for GLBA, NIST CSF 2.0, NIST 800-171, CIS Controls, and HIPAA cut the time from new framework requirement to live questionnaire, and the built-in acknowledgment workflow captures the §314.4(e) personnel attestations examiners look for.

Reports & Scorecards

Isora’s reporting layer produces reproducible artifacts for FTC compliance review, FFIEC IT examination, NCUA Part 748 attestations, and state regulator review. Examiner-grade reporting is part of the platform workflow, so evidence is ready at any point in the cycle.

Risk Management

Isora GRC’s risk register centralizes findings from §314.4(b) written risk assessments and the periodic testing required under §314.4(d). Risks publish directly from assessments with full context — owner, unit, severity, and custom fields tied to §314.4 subsections — so monitoring findings feed the §314.4(g) program-adjustment loop without manual reassembly. And the risk matrix and score distribution widgets support the §314.4(i) board reporting requirement without a standalone report build.

Inventory Management

Isora GRC works equally well for internal asset inventories and third-party risk management programs. For GLBA, the vendor inventory becomes the spine of §314.4(f) oversight — due-diligence evidence and ongoing-monitoring cadence for service providers handling customer information centralize in one system of record.

Exception Management

Isora GRC tracks documented exceptions to §314.4 controls — including compensating arrangements used where a prescribed safeguard can’t be fully implemented. Each exception carries an expiration date, owner assignment, and links to the underlying assets, applications, or vendor products, so accepted risk surfaces in §314.4(i) board reporting rather than living in a side document. Exceptions can be created manually or pushed in through the API as upstream systems flag deviations.

See the Isora GRC GLBA compliance software solution page for more information, or book a demo to start simplifying your Safeguards Rule program.

Key Takeaways

GLBA compliance software fits when it consolidates the §314.4 subsection requirements — written risk assessment, vendor oversight, training records, ongoing monitoring and incident response, plus integration with upstream HRIS, asset inventory, network monitoring, and contract management — and produces examiner-grade evidence on demand.

Vendor selection comes down to best fit before feature counts. To recap:

- Enterprise GRC is best for Fortune 500 multi-framework programs but rarely fits mid-market FIs running lean compliance teams.

- SOC 2 automation suites can supplement adjacent controls but don’t substitute for §314.4 subsection evidence under a different audit model.

- GRC Assessment Platforms™ like Isora GRC are purpose-built for the questionnaire-to-evidence lineage GLBA examination depends on, with configuration-led deployment and ease of use that survives non-GRC ownership at credit unions, community banks, and non-banking regulated entities.

The path to an examiner-ready GLBA program starts with mapping current coverage against the Safeguards Rule subsections, identifying where spreadsheets break under examination scale, and matching the platform to the staffing model that will own it on day 365.

For the regulatory deep-dive, see the Safeguards Rule complete guide; for institution-type-specific fit, see GRC software for banks and credit unions; and for platform-by-platform comparison, see Compare Isora GRC against other platforms.

Book a demo to see whether Isora GRC fits your Safeguards Rule program.

GLBA Compliance Software FAQs

Is GLBA compliance software required?

The Safeguards Rule itself does not require software. The written risk assessment, vendor oversight, training, and ongoing-monitoring requirements at §314.4 are practically infeasible to maintain at scale without one, particularly for organizations with meaningful vendor counts or customer data volumes.

What does GLBA compliance software cost?

Pricing varies by staffing model and program scope. Configuration-led, no-code platforms typically deploy without the per-seat consulting overhead that legacy enterprise GRC platforms require for multi-quarter implementations. Specific pricing is best confirmed in a demo where scope can be sized accurately.

Does GLBA apply to non-banking organizations?

Yes. The Safeguards Rule applies to entities that meet the regulatory definition of “financial institution,” which includes mortgage brokers, automobile dealers, accountants, tax preparers, and others handling consumer financial information. The FTC’s Automobile Dealers FAQ (June 2025) provides industry-specific guidance that extends to other non-bank financial institutions. The 2021 amendment expanded enforcement scope and specified subsection-level requirements at §314.4.

What’s the difference between GLBA compliance software and general GRC software?

GLBA-specific software addresses §314.4 subsection-by-subsection requirements with evidence categories that match examiner expectations. General GRC software handles framework mapping at a higher level and often lacks the Safeguards Rule-specific evidence structure that FTC, FFIEC, and NCUA examiners look for during program review.

How long does GLBA compliance software take to deploy?

Configuration-led, no-code platforms typically deploy in days to weeks. Legacy enterprise platforms span quarters. Small FIs and non-banking regulated entities rarely have the bandwidth or budget to absorb the longer timeline.

Which examiners review GLBA compliance program documentation?

The FTC reviews non-banking GLBA-regulated entities under 16 CFR Part 314. FFIEC member agencies (OCC, the Federal Reserve, and FDIC) examine banks under the FFIEC Information Security booklet. NCUA examines credit unions under Part 748, and state regulators may layer additional reviews. The platform should produce reproducible artifacts for each — see GLBA penalties and enforcement for what the failure mode looks like in practice.

This content is for informational purposes only and does not constitute legal or compliance advice. See our full disclaimer.